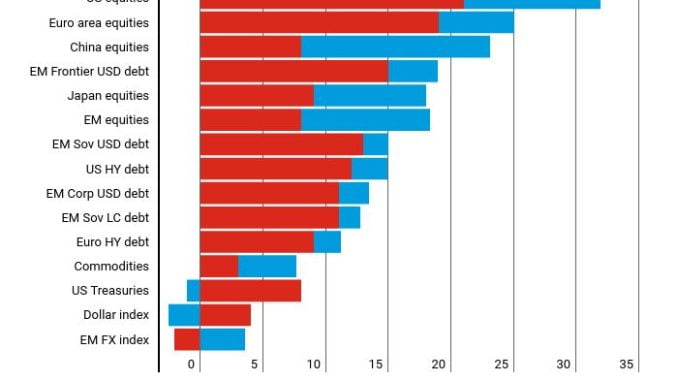

While we have seen some recent volatility, many risky asset markets around the world had a spectacular year in 2019. Equity market indices were up just over 30 percent in the United States, close to 25 percent in Europe and China, and over 15 percent in emerging markets and Japan. Emerging-market sovereign debt, U.S. high-yield debt, and emerging-market corporate debt all had returns in excess of 12 percent. Remarkably, the fourth quarter of 2019 was especially strong in China and in emerging markets.

What explains the strong performance of risky assets? One important driving force boosting asset prices was the synchronized monetary policy easing throughout 2019. As concerns about the global economy grew, central banks around the world—including the U.S. Federal Reserve and the European Central Bank—eased monetary policy through rate cuts and unconventional tools. The combined number of policy rate cuts in advanced and emerging- market economies was the largest since the global financial crisis in 2008.

The forceful response of central banks contributed to a sharp easing of financial conditions around the globe, which in turn helped contain downside risks to the global economic outlook.

The improvement in market sentiment is reflected in one of the most commonly cited indicators of downside risks, the 10-year–2-year yield curve slope, which measures the difference between yields on 2- and 10-year government debt. The slope had flattened significantly since early 2018, suggesting increasing investor concern about the economic outlook. However, the slope started to steepen again in the fourth quarter of 2019 in the United States, United Kingdom, and Germany, suggesting that investors had regained some optimism about the outlook.

The most recent WEO update discusses the easing of financial conditions and the reassessment of downside risks, and cautiously forecasts a slight rebound of global economic activity this year and next, albeit to a lower level than previously forecast. In our view, 2019 demonstrated the continuous effectiveness of monetary policy, especially when easing is undertaken in a synchronized manner around the globe. The IMF estimates that global growth would have been 0.5 percentage point lower without global monetary policy stimulus. That is a powerful outcome in the face of heightened downside risks.

Taking a longer-term view, however, the easing of global financial conditions so late in the economic cycle and the continued buildup of financial vulnerabilities—including the rise in asset valuations to stretched levels in some markets and countries, the rise in debt, and large capital flows to emerging markets—could threaten growth in the medium term. For example, default rates have increased in the U.S. high-yield market, as well as in Chinese on- and offshore corporate bond markets, albeit from low levels. Furthermore, while emerging-market spreads—the difference in yields between emerging-market debt and a benchmark such as U.S. Treasuries—are very tight for most countries, there are some specific cases where emerging-market debt is trading at distress levels, admittedly with no signs of spillovers so far.

It is therefore crucial that policy makers continue to monitor the buildup of financial vulnerabilities and take steps to address them where appropriate in order to reduce the chance that such vulnerabilities may amplify the adverse impact of shocks to the global economy. While the easing of monetary policy last year played an important role in containing downside risks to the global economy, the deployment of cyclical macroprudential policy tools, such as the countercyclical capital buffer, is now paramount to keep rising vulnerabilities from putting growth at risk in the medium term.

[“source=blogs.imf.org”]