Project finance is the financing approach typically applied to the long-term construction and development of natural resource and physical infrastructure assets. Equity and debt funding is provided upfront by multiple investors, with this financing ultimately being repaid from the cashflows of the operating assets.

Project finance in the developing world is beset by numerous risks (e.g., political and regulatory risks, operating risks, etc.). Blended finance can help address some of these challenges. Concessional financing in the form of below-market guarantees or concessional debt or equity, for example, can improve projects’ credit ratings by mitigating risk, enabling them to access private financing on better terms, while technical assistance can produce better-prepared projects at the pre-investment stage, integrating ESG considerations early on.

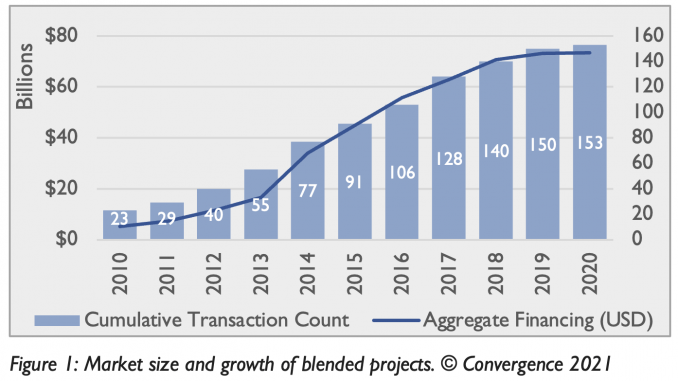

Convergence’s latest data brief analyzes the 153 blended project transactions recorded by the Convergence database (representing total committed financing of USD 73.3 billion) and presents insights from interviews with key stakeholders.

Below are some key takeaways from the Brief:

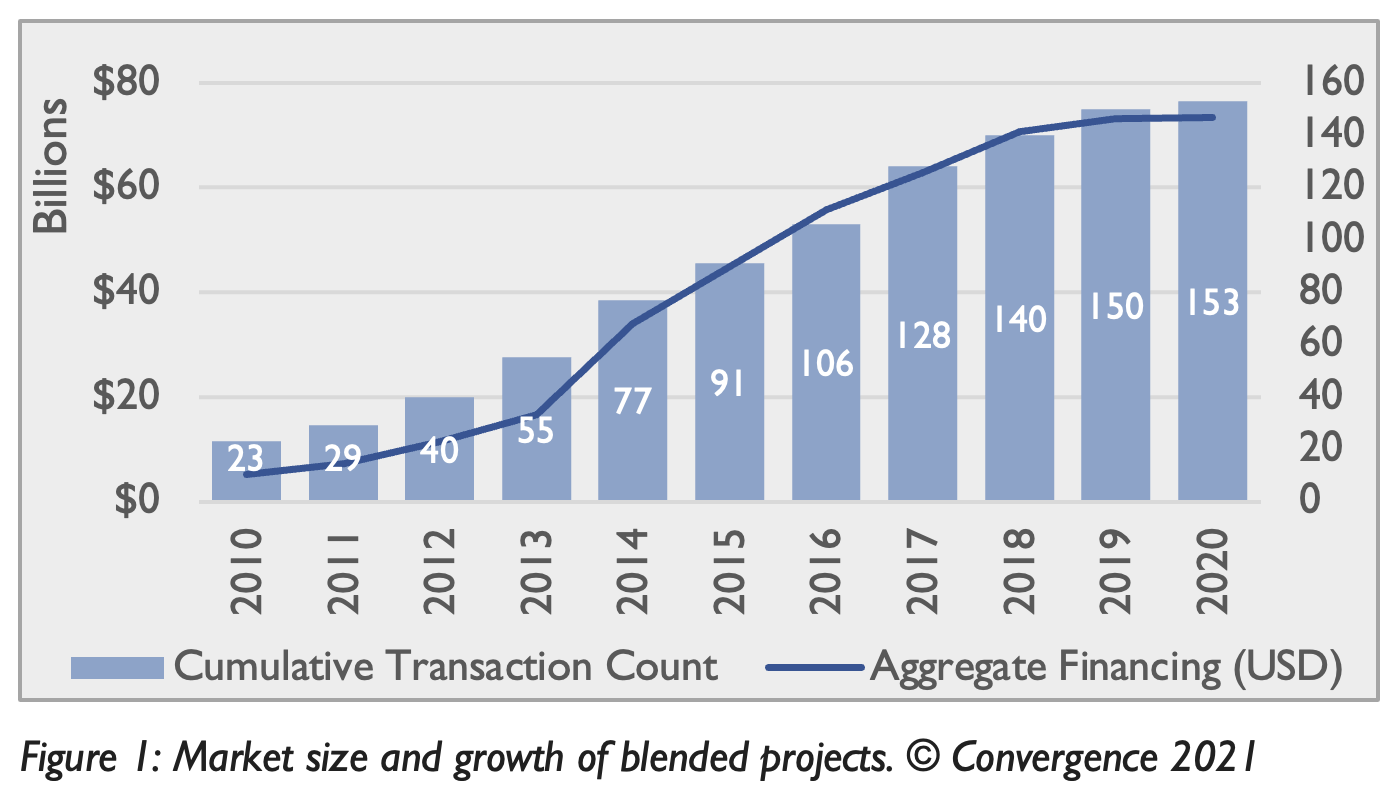

Blended finance has been effective at mobilizing private investors into large projects. Projects have a larger deal size compared to other blended structures (median size of USD 115 million), a good indication for scale:

Most projects in our dataset target renewable energy (42% of projects), energy efficiency (17%), and natural gas (10%). With energy and infrastructure projects typically being large-scale, projects have a median size of USD 115 million (vs USD 58.6 million for all transactions), with 55% of them being over USD 100 million in size (vs 38% of all). For example, the USD 7.7 billion Sankofa Gas Project looks to increase the availability of natural gas for clean power generation in Ghana, and was backed by a USD 500 million World Bank payment guarantee and USD 217 million of MIGA political risk insurance cover.

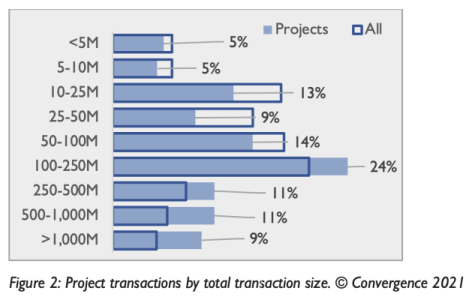

Convergence has previously noted that development guarantees have most frequently been used to mobilize additional private sector investment for larger ticket sizes (i.e., USD 100 million and above), partly because guarantees appear more in projects than in the overall market (48% vs 31%). Guarantees have various advantages: they can (i) bridge the gap between perceived and actual risk (funds are only disbursed in the event of payment default) and thereby mobilize private capital by protecting project investors from risks they’re unwilling to bear; (ii) promote capital efficiency for issuing public institutions (i.e., capital is only disbursed in the case of losses); and (iii) mobilize local currency resources. However, according to our respondents, they can still be more broadly used, particularly in a world where governments are looking for alternative sources of liquidity and to lower their cost of funding.

Technical assistance is underutilised; project preparation grant funding to support host governments, alongside standardised and bankable project documentation, is needed for scaling:

Technical assistance can be key to project development, but it appears in projects less frequently than in the wider market (17% vs 32%). Others have observed the large gaps in accessing early-stage risk financing for project preparation (e.g., the DBSA Project Preparation Fund looks to finance the preparation of infrastructure projects that fall short of the needs of the public and private sectors), with the recognition that inadequate project preparation has been among the main impediments to attracting private financing into sectors like infrastructure. Likewise, our respondents noted the challenge posed by poorly prepared projects, the need for open and competitive tendering procedures, and the key role that MDBs and DFIs need to play in providing transaction advisory support to host governments, working with them to improve the bankable suite of standardised project documentation, and thereby helping the commercial market finance projects more easily.

Infrastructure projects generally don’t specify women as end beneficiaries, though awareness of how a gender lens can improve projects’ development outcomes and risk-adjusted returns is growing:

Most projects (64% vs 36% of all transactions) target the general population as end beneficiaries, while women appear as end beneficiaries in only 8% of projects (vs 15% of all transactions). Examples of projects specifying women as end beneficiaries include the Café Selva Norte Project in Peru, which looks to improve the sustainability of local coffee value chains partly by funding the construction of a processing plant, using technical assistance to bolster female leadership and gender equality.

[“source=.convergence.finance”]